ABLE Accounts were created after the passage of The Stephen Beck, Jr. Achieving a Better Life Experience (ABLE) Act (Division B of PL 113- 295). They are an investment account similar to a 401(k) or a 529 college savings account. Contributions to ABLE accounts are made on an after-tax basis, and earnings from ABLE funds grow tax-deferred and are tax-free if used for qualified disability expenses. Anyone can contribute to an ABLE account, including the account owner, an employer, family members, and friends. Contributions to an ABLE account are not tax-deductible, but some states may allow state income tax reductions for contributions to an ABLE account. The individual with a disability is the owner of the account, but legal guardianship and powers of attorney do permit others to control ABLE funds if the owner is unwilling or unable to manage the account.

About ABLE Accounts

ABLE Accounts were created after the passage of The Stephen Beck, Jr. Achieving a Better Life Experience (ABLE) Act (Division B of PL 113- 295). They are an investment account similar to a 401(k) or a 529 college savings account. Contributions to ABLE accounts are made on an after-tax basis, and earnings from ABLE funds grow tax-deferred and are tax-free if used for qualified disability expenses. Anyone can contribute to an ABLE account, including the account owner, an employer, family members, and friends. Contributions to an ABLE account are not tax-deductible, but some states may allow state income tax reductions for contributions to an ABLE account. The individual with a disability is the owner of the account, but legal guardianship and powers of attorney do permit others to control ABLE funds if the owner is unwilling or unable to manage the account.

ABLE Resources

NDSS Resources

ABLE Policy and Advocacy

NDSS played an instrumental role in the passage of the original ABLE Act of 2014 and continues to be a leader in advocacy efforts related to ABLE accounts. After the passage of the original ABLE Act, several key provisions known as “ABLE 2.0” were implemented to further expand and improve ABLE Accounts. Most recently, NDSS was pleased to support the passage of ABLE Age Adjustment Act of 2019 to expand access to ABLE accounts for individuals with disabilities who acquire their disability after age 26. NDSS is committed to continuing to advocate for legislative priorities that ensure ABLE accounts are expanded and are an accessible tool to support individuals with disabilities in working, earning, and saving for their futures.

For more information, please contact our team at policy@ndss.org. To learn more about NDSS’ grassroots advocacy initiatives, please visit our DS-Ambassador page here.

Federal ABLE Advocacy Resources

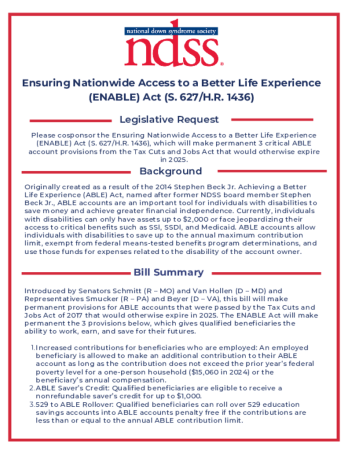

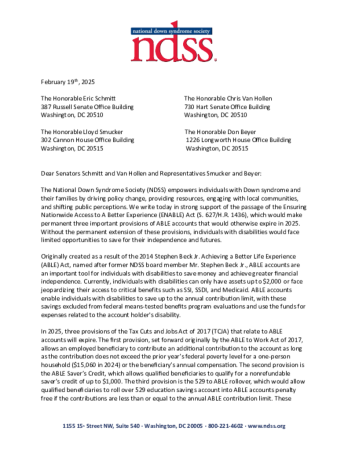

ENABLE Act

On July 4, 2025, the provisions of the Ensuring Nationwide Access to a Better Life Experience (ENABLE) Act were signed into law as part of the One Big Beautiful Bill Act.

NDSS championed the ENABLE Act in the 119th Congress. The bill, now passed into law, made three key provisions from the 2017 Tax Cuts and Jobs Act permanent, including increased contributions to ABLE accounts for individuals who have a job, the continuing of savers tax credit, and rollovers from traditional 529 accounts to ABLE accounts. The ENABLE Act ensures that individuals with Down syndrome can continue to take advantage of these critical provisions to save for financial independence and disability-related needs.

NDSS routinely shares information about the ENABLE Act and other relevant legislation on our social media accounts. Be sure to follow along and share these posts on your own personal channels!

Additional ABLE Legislation

NDSS continuously monitors additional legislation to improve and expand access to ABLE accounts being introduced in Congress. When these bills are introduced, they will be linked below. If you have any questions, please contact policy@ndss.org.